FINRA Named It. The Rules Were Already There.

Last week, we examined how FINRA's 2026 Annual Oversight and Regulatory Report made AI-generated marketing content a supervisory priority for the first time. The report named marketing as a GenAI use case, expanded its review scope from three to fifteen, and set out expectations for written supervisory procedures that specifically address AI tools.

FINRA was the first regulator to name it explicitly. However, the underlying obligation is not new, and it is not limited to one jurisdiction. Financial services regulators in the United Kingdom, Canada, Australia, New Zealand, and the European Union already have marketing compliance frameworks that apply to AI-generated content. Most of those frameworks predate generative AI by years.

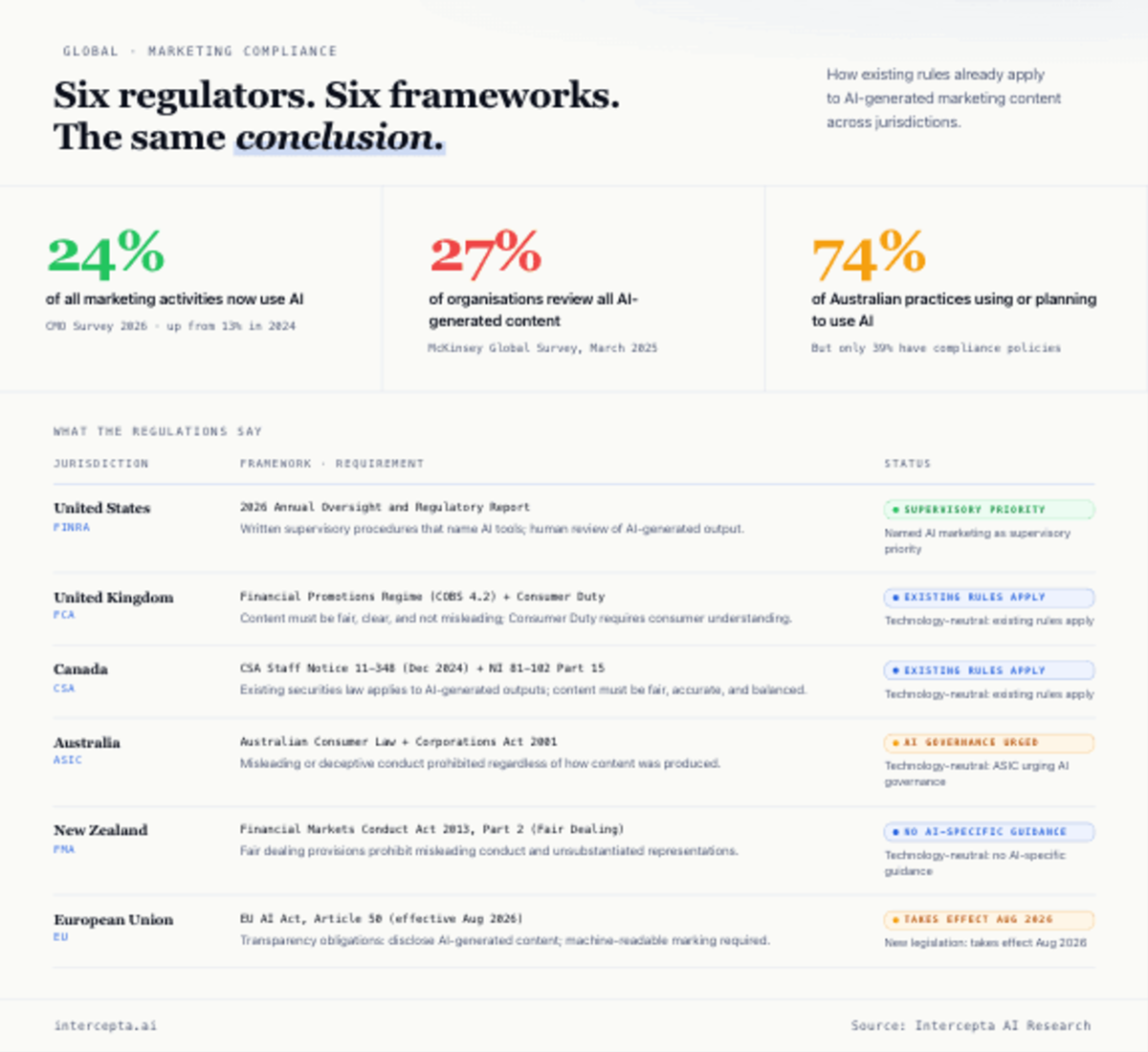

The rules have not changed. AI adoption in marketing has. According to the 2026 CMO Survey, AI now powers 24% of all marketing activities, nearly doubling from 13% two years earlier, with marketing leaders projecting it will reach 56% within three years. Yet, McKinsey's global survey found that across all business functions, only 27% of organisations using generative AI review all of the content those tools produce before it is used. The tools now producing regulated content do not know which rules apply, and the teams reviewing it often cannot match the speed of production.

This article examines what those existing obligations require in each market, and where the gap between AI adoption and compliance oversight is widest.

The Financial Conduct Authority Has No AI Rulebook. It Does Not Need One.

The FCA has taken a different approach from FINRA. It has not introduced AI-specific rules for marketing content and has said explicitly that it does not intend to. The FCA's position, reaffirmed in evidence to the Treasury Committee, is that its existing framework already applies to AI-generated content. The Consumer Duty, the financial promotions regime, and the Senior Managers and Certification Regime do not distinguish between content written by a person and content produced by an AI tool.

That does not mean the FCA is standing still. It has been actively enforcing against non-compliant financial promotions, including content generated or disseminated using AI tools. In January 2026, it launched a long-term review into AI and retail financial services led by Executive Director Sheldon Mills, reporting to the FCA Board in summer 2026. The House of Commons Treasury Committee has gone further, recommending that the FCA publish comprehensive AI guidance for firms by the end of 2026. Whether or not the FCA adopts that recommendation, the political expectation is moving ahead of the current regulatory position.

The financial promotions regime gives the FCA a specific, rules-based framework for marketing content. Under COBS 4.2, all financial promotions must be fair, clear, and not misleading. Benefits must not be presented without appropriate prominence for risks. Past performance must comply with COBS 4.6. Required risk warnings must be present and must not be diminished by the surrounding content. In April 2026, CP 26/15 proposed consolidating consumer credit promotions under the Consumer Duty framework, and the Consumer Duty itself raises the bar further by requiring firms to demonstrate that consumers actually understand their communications (FCA, Consumer Understanding: Good Practice and Areas for Improvement, March 2026). The FCA required firms to amend or withdrawl nearly 20,000 non-compliant financial promotions in 2024, up from 573 in 2021.

For marketing teams, the FCA's financial promotions rules require content to be fair, clear, and not misleading under COBS 4.2. That standard applies regardless of how the content was produced. If an AI tool drafts a credit card balance transfer promotion that highlights the 0% introductory rate but presents the reversion rate and transfer fee in a way that diminishes their prominence, the content may breach that standard. Whether the content was drafted by an AI tool or a copywriter, the compliance question is the same: does the reversion rate have appropriate prominence relative to the introductory rate? That is a rules-based question, and the content should be validated against the rule before publication.

For compliance teams, the financial promotions regime creates specific requirements that can be validated against the rule. Required risk warnings must be present. Benefits and risks must be balanced. Past performance must be presented in accordance with COBS 4.6. The Consumer Duty raises the bar further by requiring firms to demonstrate that these communications achieve the consumer understanding outcome, but the starting point is whether the content meets the specific rules that apply to it.

Existing Securities Law Already Applies to AI-Generated Content In Canada

The Canadian Securities Administrators published CSA Staff Notice 11-348 in December 2024, addressing the applicability of Canadian securities law to the use of artificial intelligence systems in capital markets. The notice clarifies that existing securities legislation applies to AI-generated outputs and poses questions on whether current supervisory approaches should be adapted. The Canadian Investment Regulatory Organisation (CIRO), formed in January 2023 through the merger of IIROC and the MFDA, is harmonising compliance rules into a single framework. In Québec, the Autorité des marchés financiers (AMF) published its Guideline for the Use of Artificial Intelligence in April 2026, setting out expectations for financial institutions on AI use, effective 1 May 2027. Canada does not yet have standalone AI legislation. However, the CSA has made clear that the absence of an AI-specific statute does not create a regulatory gap. Existing securities law applies to AI-generated content in capital markets.

For marketing and compliance teams operating in Canada, the principle is the same as in the United Kingdom. If an investment dealer uses AI to draft a promotional email for a balanced fund, the output must meet the same standard as any other sales communication under NI 81-102 Part 15: fair, accurate, and balanced. If the AI tool highlights the fund's strong 12-month return without presenting longer-term performance that was less favourable, or omits the required cautionary language about past performance, the sales communication is misleading under the same rule it would breach if a human analyst had written it.

For compliance teams, the practical question is whether the firm's existing review process catches AI-generated omissions before publication. If the firm cannot demonstrate that the content was reviewed against the applicable securities disclosure requirements, the method of production does not change the exposure. The CSA's position is that the obligation attaches to the output, not the tool that produced it.

The Governance Gap Is Quantifiable In Australia and New Zealand

In Australia, the governance gap is the most quantifiable of any jurisdiction. According to Adviser Ratings research from October 2025, 74% of Australian financial advice practices are now using or planning to use AI, surging from 45% the year before. But only 39% have policies or guidance on how to use it compliantly.

The Australian Securities and Investments Commission (ASIC) has made its position clear. ASIC's 2025–26 Corporate Plan places a strong focus on enhancing AI oversight. In a Letter to Industry dated 8 May 2026, ASIC urged all licensees and market participants to urgently strengthen resilience in the face of frontier AI models. While focused on cyber resilience, the letter reinforced the principle that AI governance is a board-level obligation, not a technology workstream, and that existing licensing obligations apply to AI-driven risks across the business.

ASIC and the Australian Prudential Regulation Authority (APRA) have both issued calls to action on AI governance to their regulated entities. Australia does not have a standalone AI Act. AI is governed through existing technology-neutral legislation, including the Privacy Act 1988, Australian Consumer Law, and the Corporations Act 2001. From December 2026, amendments to the Privacy Act will introduce new obligations for automated decision-making.

New Zealand's Financial Markets Authority operates a technology-neutral framework. The fair dealing provisions under Part 2 of the Financial Markets Conduct Act 2013 prohibit misleading or deceptive conduct and unsubstantiated representations in relation to financial products, regardless of how the content was produced. The FMA has confirmed that the same legal obligations apply whether content is delivered digitally or in person. The FMA has not issued AI-specific guidance for marketing content, but existing fair dealing requirements apply to AI-generated output on the same basis as any other material.

For marketing and compliance teams in both markets, the regulatory expectation is consistent with every other jurisdiction covered in this article. The obligation is on the firm, not the tool. If a firm publishes content that does not meet the applicable standard, the method of production is not a defense.

The Pattern Extends Beyond the US, UK, Canada, Australia and New Zealand

The European Union is moving in the same direction. The EU AI Act, the first legislation anywhere to impose specific transparency obligations on AI-generated content, takes effect on 2 August 2026. Article 50 requires firms to disclose AI-generated content and mark it in a machine-readable format. A broader framework for high-risk AI systems in financial services, covering risk management, data governance, human oversight, and documentation, follows in December 2027.

The regulatory direction is consistent across every jurisdiction covered in this article. In most cases, the obligation is not new. The difference is that AI tools are now producing regulated content at a speed and scale that existing review processes were never designed to handle.

The Compliance Obligation Is Structural, Not Jurisdictional

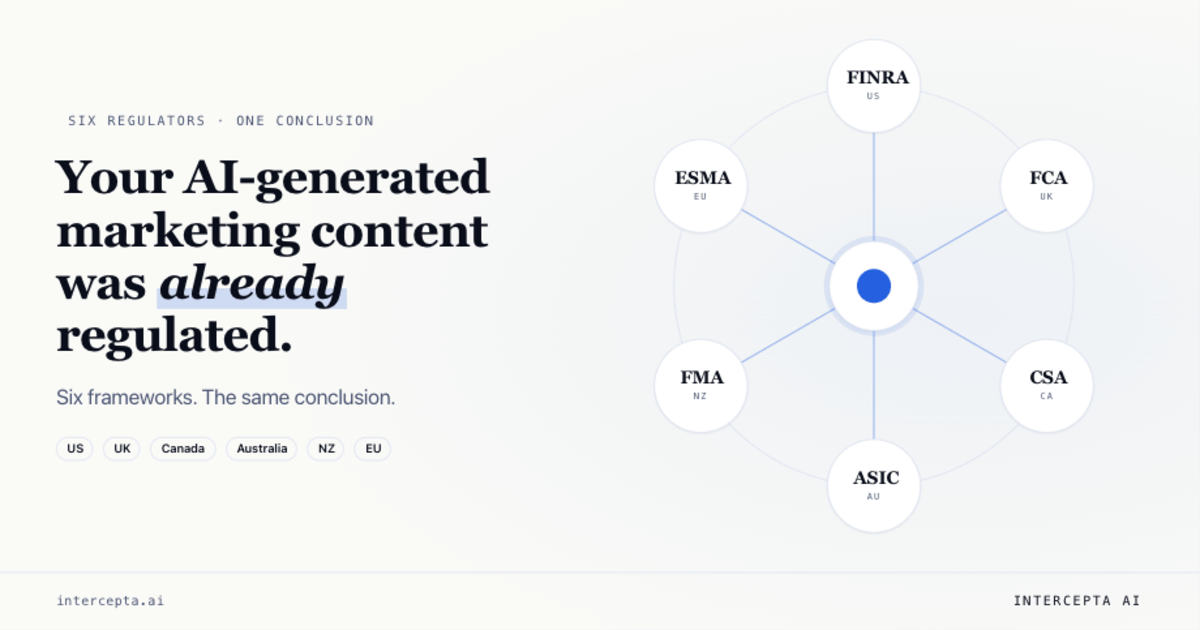

Six regulators. Six different frameworks. The same conclusion.

FINRA expects written supervisory procedures that name AI tools and require human review of output. The FCA expects marketing content to meet the fair, clear, and not misleading standard under its financial promotions regime, with the Consumer Duty raising the bar on top of that. The CSA has confirmed that existing Canadian securities law applies to AI-generated content without modification. Under Australia's technology-neutral framework, existing consumer protection and financial services legislation applies to AI-generated marketing content, and ASIC has called on all licensees to strengthen AI governance as adoption outpaces oversight. The FMA applies its fair dealing obligations to AI-generated content on the same basis as any other material. The EU AI Act introduces transparency and disclosure obligations that take effect from August 2026.

None of these regulators coordinated their timelines. They did not adopt identical frameworks, but they are all responding to the same structural reality. AI tools are producing marketing content faster than compliance teams can review it, and the regulatory obligation to review that content has not changed.

The question for firms operating across borders is not whether any one of these frameworks applies. It is how many apply at the same time.

The operational requirement across all six frameworks is the same. A firm must be able to show that its marketing content was reviewed against the applicable regulations before publication, that the review was documented, and that the process holds when a regulator in any of those jurisdictions asks to see the record.

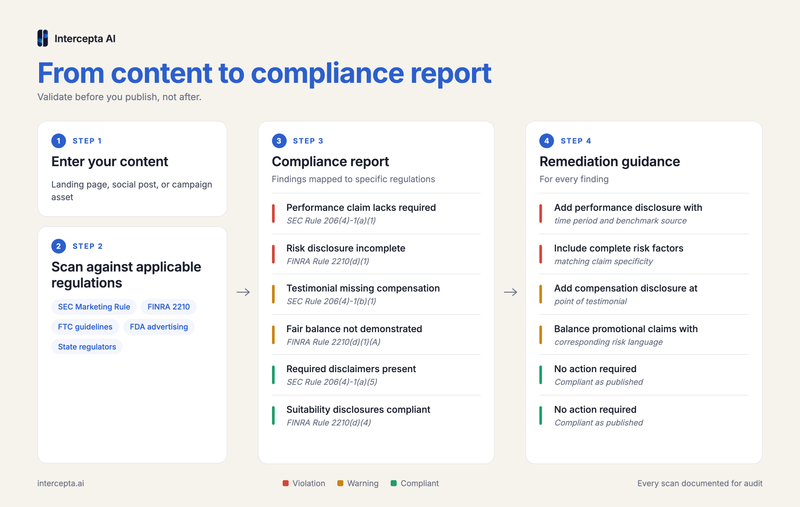

Intercepta AI validates marketing content, before and after publication, against regulatory rules across US federal and state regulations, UK requirements, EU rules, Canadian securities standards, Australian financial services obligations, and New Zealand fair dealing requirements. Marketing teams get remediation guidance before content goes live. Compliance teams get a documented regulatory record and automatic re-validation when regulations change.

Check out https://blog.intercepta.ai/ai-generated-marketing-content-is-now-a-finra-supervisory-priority/ as the precursor to this article.

Try Intercepta AI

Your first three scans are free at intercepta.ai.

No payment method required.

Sources

- FCA, Consumer Understanding Report, March 2026

- FCA, Consultation Paper CP 26/15: Financial Promotions for Consumer Credit Under the Consumer Duty, April 2026

- FCA, Financial Promotions Data 2024; Annual Report and Accounts 2024-2025 (nearly 20,000 non-compliant promotions amended or withdrawn, up from 573 in 2021)

- FCA, Financial Promotions Quarterly Data and Enforcement Activity, 2024–2026

- FCA, Long-term Review into AI and Retail Financial Services (Sheldon Mills), launched January 2026

- House of Commons Treasury Committee, AI in Financial Services Report, January 2026

- EU AI Act, Article 50: Transparency Obligations for Providers and Deployers of Certain AI Systems (enforceable 2 August 2026)

- EU AI Act, Articles 9–15: High-Risk AI System Obligations (delayed to December 2027 per Digital Omnibus agreement, May 2026)

- Canadian Securities Administrators, CSA Staff Notice 11-348: Applicability of Canadian Securities Law to the Use of Artificial Intelligence Systems in Capital Markets, December 2024

- Canadian Investment Regulatory Organisation (CIRO), formed January 2023 (IIROC + MFDA merger)

- Autorité des marchés financiers (AMF), Guideline for the Use of Artificial Intelligence, published April 2026, effective 1 May 2027

- ASIC, 2025–26 Corporate Plan

- ASIC, Letter to Industry, 8 May 2026

- ASIC and APRA, Calls to Action on Artificial Intelligence, May 2026

- Adviser Ratings, 2025 Australian Financial Advice Landscape Report, October 2025 (74% of practices using or planning to use AI, up from 45%; 39% with compliance policies)

- Privacy Act 1988 (Australia), amendments effective December 2026 (automated decision-making obligations)

- Financial Markets Authority (New Zealand), Fair Dealing Obligations under the Financial Markets Conduct Act 2013

- FCA Handbook, COBS 4.2: Fair, Clear and Not Misleading Communications Rule

- FCA Handbook, COBS 4.6: Past Performance

- Duke University / Deloitte / American Marketing Association, The CMO Survey, 34th–35th editions (2025–2026): AI powers 24.2% of marketing activities in 2026, up from 13.1% in 2024; projected 55.9% within three years (n=308)

- McKinsey & Company, "The State of AI: How Organizations Are Rewiring to Capture Value," Global Survey, March 2025 (27% of respondents whose organisations use gen AI review all content before use)